Narrative Wedge: Profit and Survival Guide

Sep 19, 2024 06:36:34

Original Title: The Narrative Wedge

Original Author: JOEL JOHN

Translated by: Deep Tide TechFlow

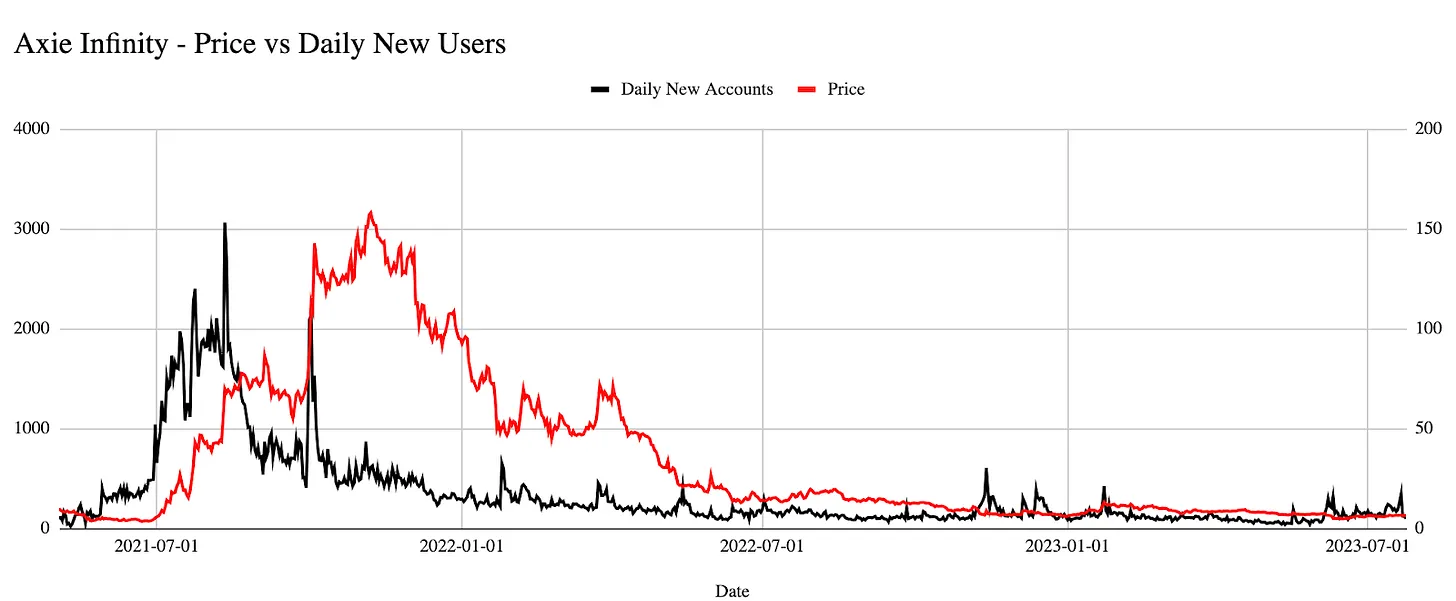

Over the past week, I had an observation. You could invest in Axie Infinity at the start of the gaming craze, then leave, and come back to find your returns were greater than those of most venture capitalists in Web3 gaming. Axie's price once fell to $0.14 and has now risen to $6, yielding a 40x return.

At its peak, it was over 1000x. The reason is that most seed-stage venture capital projects in Web3 gaming are either far from liquidity or may falter before raising more funds in the current market environment. But there are some flaws in my thinking:

- Seed-stage venture capital projects should not expect returns within an 18-24 month timeframe.

- I assumed investors allocated funds to Axie Infinity while the game was still an unnoticed narrative.

However, the underlying logic remains that you can invest in a liquid asset during a bear market and achieve better returns than in early-stage venture capital deals of that narrative. This dilemma has led me to reflect on the risk spectrum in cryptocurrency and how attention precedes venture capital. This article summarizes my thoughts on how narratives drive funding and attention in our industry.

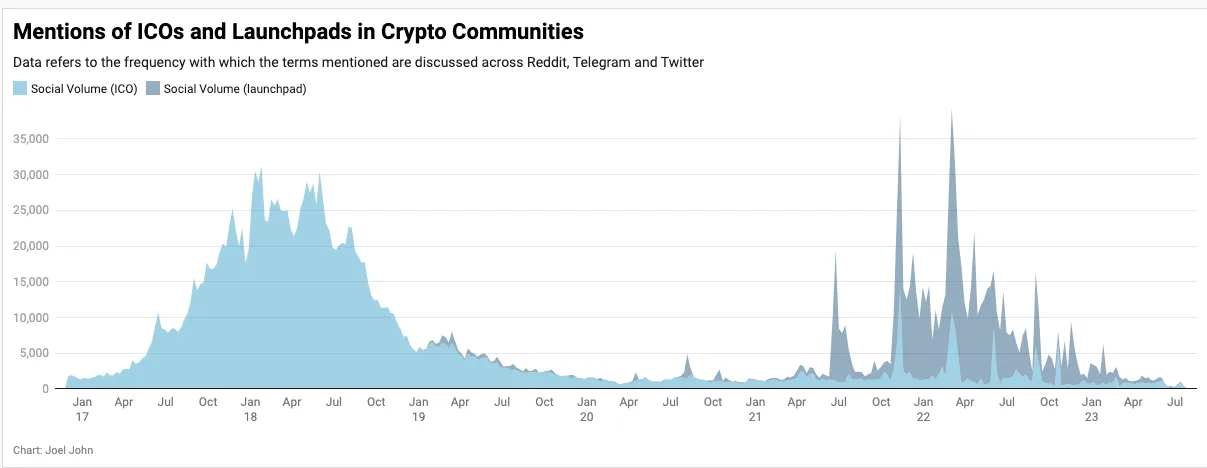

Before we begin, let’s look at some numbers. According to the data product I use, among over 3,500 tokens, nearly 1,300 had fewer than 10 wallets transferring in the past month. Among the 14,000 dApps tracked by DappRadar, fewer than 150 have 1,000 users. In this industry, our focus quickly shifts from one asset to another. We see a similar situation with our confidence in fundraising mechanisms. The data below shows the mentions of ICOs and issuance platforms in well-known cryptocurrency communities over the past few years.

If you were in the space back in 2017, you might have thought venture capital would change forever. Many of the startups that raised funds in that market no longer exist. According to data sources, cryptocurrencies raised between $19 billion and $60 billion from retail and institutional participants that year. However, the survival rate of that batch of ICO projects is comparable to what we traditionally see with startups.

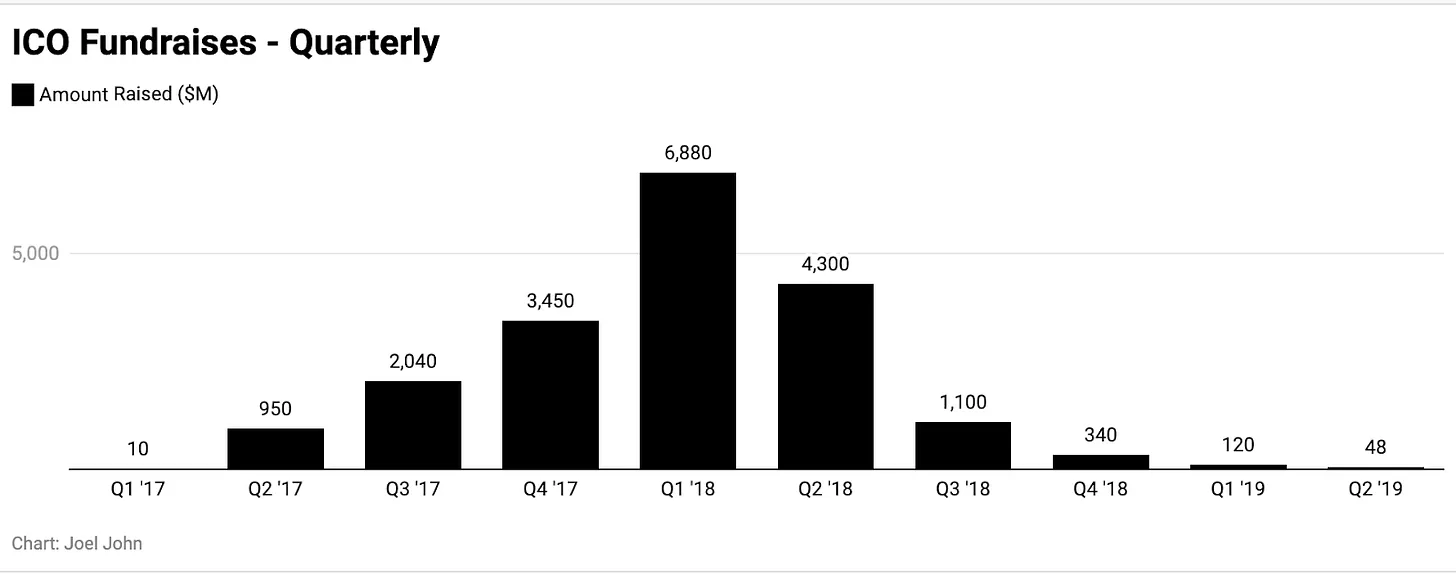

You can see the results between January 2019 and January 2021 in the chart above—this was the golden age of cryptocurrency venture capital. Interest in ICOs quickly faded. Investors saw an opportunity for a brief period when those dream-filled founders could no longer attract retail capital to build. Startup valuations were between $5 million and $10 million. Founders and investors had to collaborate anew to survive.

One reason founders turned to VCs for funding is a better understanding of the risks of prematurely issuing tokens. You have to spend time managing the community, doing legal work to ensure compliance, and tying your net worth to a liquid asset while running a company. Founders might become frustrated by comments from someone on Discord about team members and decide to dump all their tokens on an exchange with only $10,000 in liquidity, waking up to find they are 20% poorer.

Years have passed, and we are back in the season of Launchpads—exchanges play the role of gods, deciding which venture capital projects can raise millions from retail. While there are many barriers this time, at least they ensure that retail investors receive better terms than the billions in valuations seen in 2017 ICOs.

I chose the case of ICOs giving way to Launchpads because there is relevant data. Enough years have passed since the ICO boom that we can look back and understand what happened. If you look at some of the newer themes like DeFi, NFTs, or Web3 gaming, you will find that public interest in them has completely vanished.

But unlike ICOs, the stories of DeFi, Web3 gaming, and NFTs are still evolving.

The Gradual Decline of Narratives

DeFi has shifted from a peak of over-expectation to a phase of enlightenment. Uniswap competitors have not emerged. Aave and Compound dominate the lending market (for spot and over-collateralized assets). The continuous iteration of these products will be more consumer- or institution-focused and no longer overly obsessed with speculation.

Robert Leshner has shifted focus to launching a mutual fund, while Stani has turned to Lens (Web3 social), showing how founders who have been in the industry are preparing for the next round.

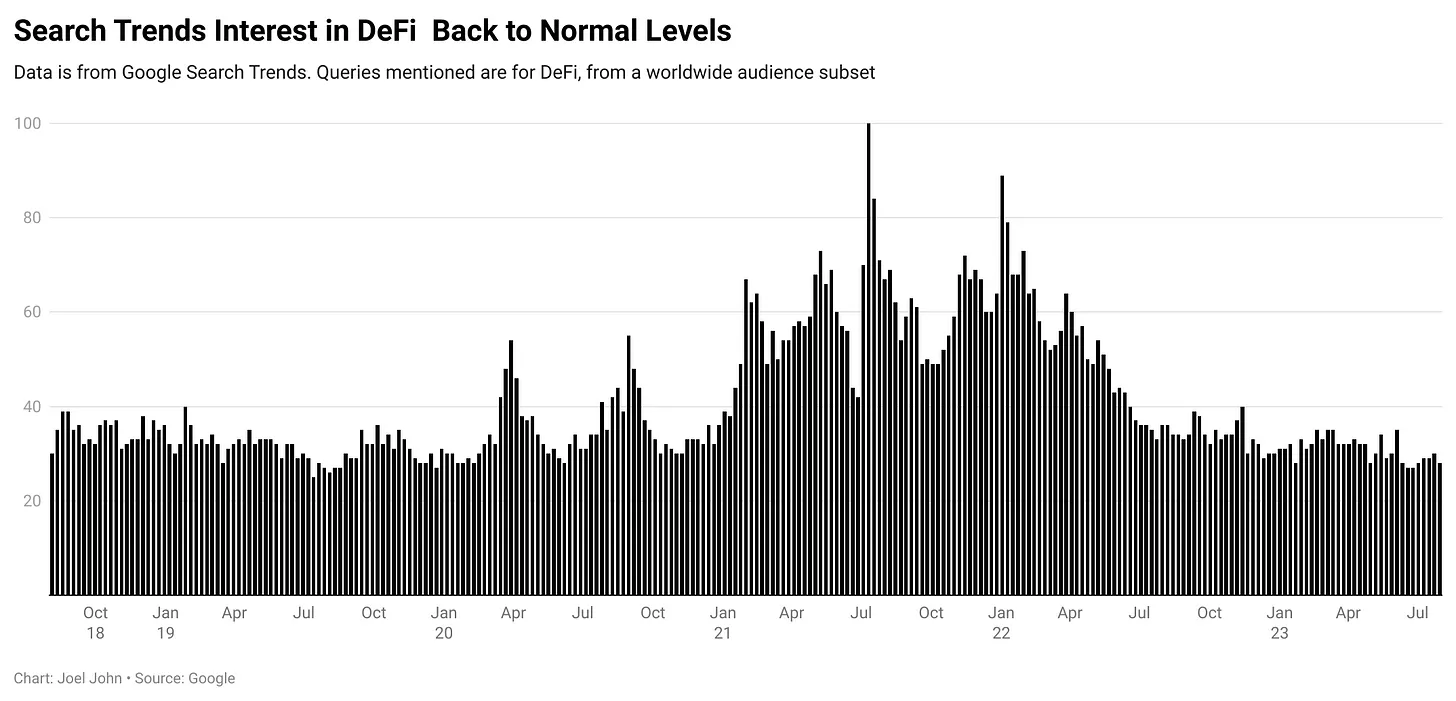

Google search trends, TVL, and user numbers are good indicators of attention and capital flow in DeFi. As of now, the funds on DeFi platforms have dropped from a peak of $160 billion to a low of $40 billion.

If you look at the user number data, it has decreased by 50% over the past few months. But compared to when DeFi Summer just started in March 2020, the user count has still grown 100 times.

In other words, while interest and usage have decreased, the number of users within these product categories still far exceeds previous levels. However, if you look at the search trends for the same functionalities, you will see a completely different story.

Interest has returned to 2018's bear market levels. It’s as if no one cares about the industry anymore. I checked the data for NFTs and ChatGPT, and they show similar trends. Searches for aliens are on the rise. (Maybe we need to start investing in alien service businesses.)

From the DeFi data, I have a few observations.

- Narratives build momentum at the start of a bull market.

- They are usually driven by technological developments.

- Early participants in specific areas receive outsized returns as narratives and usage scale simultaneously.

- Compound, UniSwap, and Bored Apes are examples where the narrative windfall combined with product usage delivered outsized returns for investors.

The challenge is that you must invest in narratives that may disappear before they attract enough users. We may need to revisit Axie Infinity to untangle this.

Timing is Everything

I return to Axie because it encapsulates several themes well.

- By 2021, Axie had been listed and had undergone about two years of product development.

- It could be said that it was undervalued at that time.

- Axie marked the beginning of the Web3 gaming narrative.

It’s important to note that this is not an evaluation of Axie. I am optimistic about what the team can achieve, and we have been researching arguments about Web3 gaming internally. I remain a loyal fan of Sky Mavis and their work on consumer-grade blockchain applications. Our focus is on price and user activity.

If you pay attention to the chart above, you will see that before Axie's price surged to $150, there was a significant influx of users. On-chain investigators likely saw the extent of new users entering the product and priced it well before July 2021.

But by October, as the number of new users began to decline, Axie became more of an asset than a product. This is a trap that all on-chain products can easily fall into. The super-financialization of in-game assets means that hedge funds in New York can pay a guild member struggling in the game. The model of earning in-game yields relies on the inflow liquidity of in-game assets. Sometimes, this liquidity comes from speculators and institutions.

Between July 2021 and January 2022, many investors formed beliefs while waiting and wrote papers on how the industry would develop. Founders also realized the difficulties in building DeFi dApps and believed gaming was the next big trend. Just as many founders today are venturing into artificial intelligence.

The real risk lies in the 18 months following January 2022. Did you notice the steady decline in new user numbers in the chart above? This is the shrinking user base of all Web3 native gaming applications. Tools built on the margins, like "Steam for Web3 games," quickly find it hard to attract users.

This misunderstanding of short-term price spikes versus actual consumer demand is a trap many founders fall into. The risk for founders is that without attraction, it is difficult to secure follow-on funding in the current market environment.

Founders are likely to miss the right timing in the right market. The danger for founders is shutting down their business before enough attention or capital flows into the category.

As a venture capitalist, on one hand, you see liquid markets providing huge returns to traders, while on the other hand, you will compete with a group of founders who are also venturing into that theme. This is not a pleasant experience for any participant.

My points are:

Markets often price narratives in the short term.

Given the liquidity characteristics of Web3 investments, liquid assets may exit in a quarter.

Given the illiquidity characteristics of venture capital, startups may not have a market to tap into when products go live, as products need time to develop.

This often means chronic death and gambling on user returns. Products effectively become a bet on a "bull return."

The exception is when a category expands to have enough interested users, and you build something unique. Ironically, DeFi has crossed that chasm. At a scale of 3 million users, founders building in DeFi no longer worry about new users entering the market.

Crypto-native investors in venture capital are either appreciators or pioneers. They either have the distribution and influence to create a new category or the foresight to realize a whole new industry is emerging. If they rely solely on price action as a driver to formulate new arguments, then their timing for entering the market is very late. They likely won’t see exit opportunities unless it’s a business that can scale to an IPO or be acquired. And both scenarios are rare in the token space.

Another way to influence founders is through the evolution of business models. For example, due to the emergence of royalty-free markets like Blur, the effective royalty rate for NFTs has dropped from about 2.5% to 0.6% over the past year. As of this writing, about 90% of NFT transactions do not charge any royalties.

Essentially, this means that any business built on the premise that a large number of traditional artists would enter the industry, who in turn need tools to generate income, will completely disappear. Last year, as the model shifted, countless creator economy businesses had to pivot.

For all emerging technologies, chaos is a way of life in the crypto world.

Free

Let’s take a step back to the late 2000s. After a long day at school, you log into Facebook to chat with friends. There are countless entertaining videos on YouTube. Ads are sprinkled throughout these activities, but you rarely pay a dime for them. The internet had formed habits before you paid.

In contrast, Web3's obsession with ownership and exclusivity has created a small-scale user base. According to their blog, Arkham Intelligence has over 100,000 users. Nansen's V2 product has registered over 500,000 users today. Dune has one of the largest communities of data scientists in the industry. They all have one thing in common: free.

The genius of the internet lies in letting users bear the cost of most actions. In return, it gained influence. The great danger of Web3 is how high the cost is for each interaction. For users who do not need online socializing, spending $8 to buy an image on the blockchain is not appealing.

For users who have had free email addresses for decades, why spend $50 on ENS? Axie Infinity initially required $1,200 to purchase an NFT to play the game. The guild model relied on this high barrier. Last year, they released a free-to-play version, realizing the dangers of maintaining such a high threshold.

Today, Reddit combines this "free" and "owning" very cleverly. As a social network with 400 million monthly active users, Reddit is a giant. So far, about 15 million wallets have collected their collectibles. This is roughly double the number of DeFi users during peak months. Accounts with specific years and characteristics are allowed to purchase collectibles from Reddit.

In this case, most users still use "free" products, with only a small portion of users minting, trading, and owning collectibles. Distribution is a problem solved by a website that has been running for 18 years.

Rabbithole and Layer3 fit this model very well. They do not charge users but provide value to those curious enough to explore new opportunities on-chain. According to a tweet from Layer3's founder, the product has provided about 15 million on-chain operations for those interested in cryptocurrency.

Product strategy shifts are already happening. If you visit Beam.eco, you will see a wallet set up in less than 10 seconds. Asset.money helps you collect NFTs with fewer than three clicks. Users do not have to worry about gas fees, entry, or setting up wallets. Of course, there are security trade-offs. This is similar to how email transitioned from everyone running their own servers to third-party servers run by providers like Hotmail and Google.

Barter Trade

Remember I mentioned that narratives alone cannot determine the timing of crypto venture capital? The way to escape this trap is the oldest trick in the book:

- Attract a user base and maintain it over the long term;

- Accumulate value steadily over a long timeframe.

Some tokens in the industry have successfully done this. When I think of DeFi, I think of Uniswap. Despite the attacks on royalties, OpenSea remains relevant. The tail end of venture capital is a big bet on how and when attention and capital flow.

The only way to break free from an unhealthy reliance on investor or speculator capital is to leverage the purest form of capital available to all businesses: the attention of their customers. As venture capital contracts, more and more startups (and protocols) will have to seek users who care about their products.

The most relevant example I found is Manifold.xyz. The product focuses on helping creators mint NFTs relatively easily. According to TokenTerminal's data, their fees exceeded $1 million last month. Is it performing well? Probably not. Is it relevant in the current market? Absolutely.

I find a common thread among many participants who have successfully weathered market cycles: their first-mover advantage. This is a recurring story.

Small teams enter an industry when market sentiment peaks. They see the market gradually shrinking. Usually, fewer than five participants are willing to continue building as competitors leave. When attention and capital return, they are the most likely to scale.

From this perspective, as long as you can survive, the narratives that big investors abandon are the ones you should engage with.

Some time ago, it was "cool" to join Web3; now mentioning that you work in this industry might feel awkward. Teams feel the need to fabricate statistics to stay relevant. We often see founders exaggerating their products by driving trading volume through airdrops.

For founders, this is a survival memo.

- Understand the difference between VCs betting on narratives and those digging deep into your sector.

- Entering the market early is a moat in itself. But it also means it may take months or longer for people to believe in your product. Most of your pitches will become investor education courses. This is both a blessing and a curse.

- In a market where all peers are going out of business, survival is the ultimate game. Keeping expenses to a minimum to survive is usually the right approach.

- Consumer attention often precedes investor capital. Engaging with users before pitching to investors helps iterate on the product.

- If product-market fit cannot be found within a meaningful timeframe, it makes sense to shut down the business.

Given that the crypto market is a highly liquid market, investing (time or money) requires understanding which stage of the narrative you are in. The trap often lies in spending years in a collapsing sector. Personally, I do not believe Web3 gaming is over. Its story is still being written by countless founders who still believe in the sector.

The trap is confusing public market price action with private market investment opportunities. When products go live, the narrative may already be dead. Follow-on funding may disappear. Consumers may not care. This is a tough battle many founders will have to face in the coming quarters.

Related Projects

Latest News

Oct 14, 2025 15:33:44

Oct 14, 2025 15:17:59

Oct 14, 2025 15:16:14