The Battle for Digital Asset Infrastructure: Where the Gap Comes From

3月 16, 2026 11:14:39

This report is written by Tiger Research and explores the key requirements and methods that financial institutions should consider when adopting digital assets.

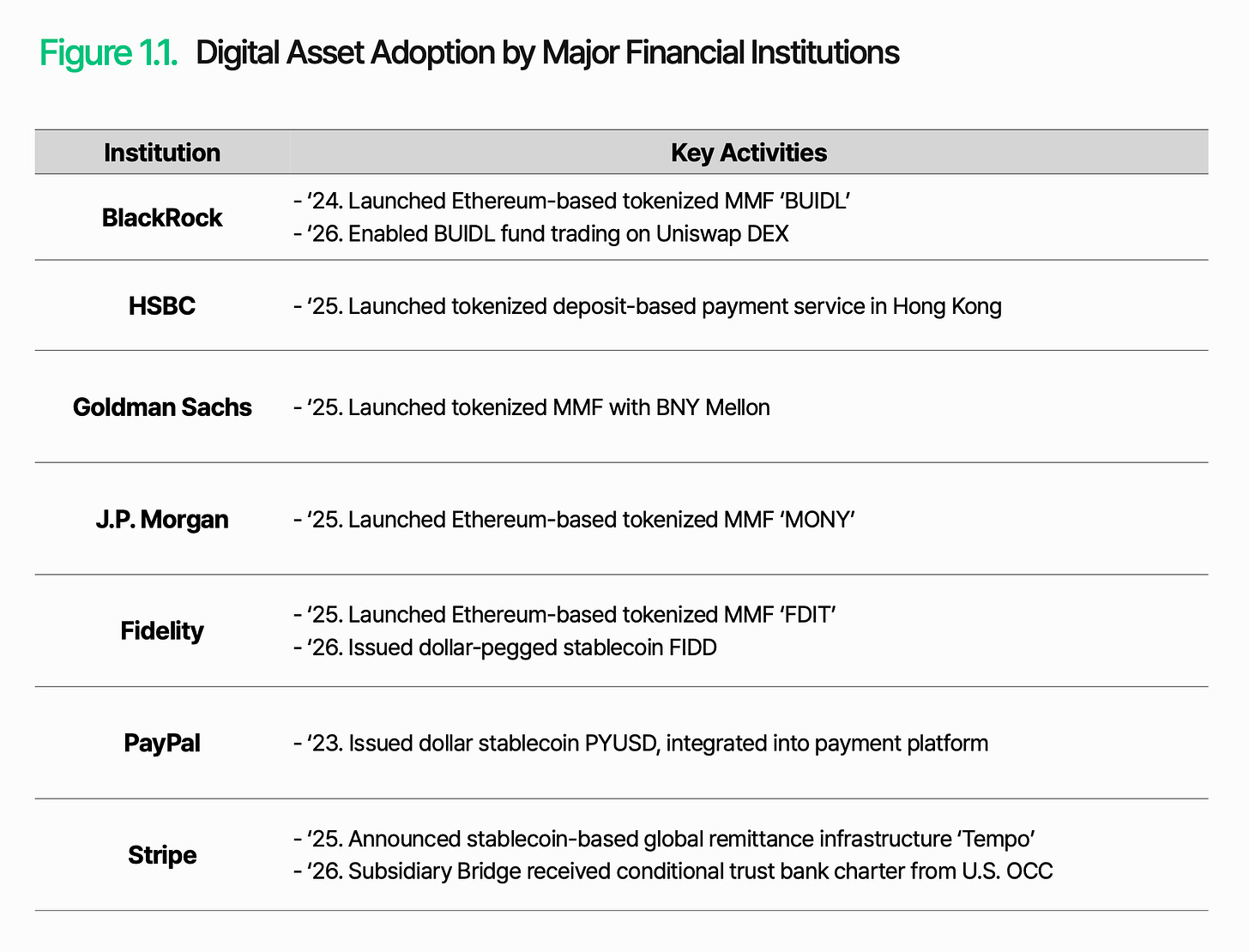

PayPal has issued a stablecoin, PYUSD, pegged to the US dollar and integrated it into its payment services. BlackRock has launched a tokenized money market fund, BUIDL, with assets under management exceeding $3 billion. JPMorgan, Fidelity, and Goldman Sachs have also followed suit. Wall Street, which stood by just two or three years ago, has now directly entered the market.

The reason is simple: the structural inefficiencies of the traditional financial system. Each transaction incurs intermediary fees, settlements take days, and trading stops when the market is closed. Digital assets fundamentally change all of this: lower costs, faster speeds, and no time constraints. The result is a more flexible and scalable market. Digital assets are no longer a question of "why," but rather "how."

However, "how to achieve this" is much more difficult than it seems. When the financial industry transitions online, the challenge lies not in technology, but in how to maintain trust and control in the new environment. This applies here as well. Issuance, custody, transfer, and settlement must all operate reliably on-chain while integrating with traditional financial systems and regulatory frameworks.

The core challenge is clear: how to enable digital assets to perform financial functions within the existing system.

1. A New Global Financial Order

Digital assets have shifted from a speculative market to an institution-led market. For a long time, institutional investors have taken a conservative stance, but the accelerating regulatory push led by the United States is changing their perspective. Today, institutional investors view digital assets as a brand new opportunity and wish to explore and seize it early.

This shift is most evident in the actions of large financial institutions. For instance, BlackRock has not stopped at tokenizing its money market fund but has also begun enabling trading of the fund on the decentralized exchange UniswapX. This indicates that global financial institutions now view digital assets as a new type of infrastructure, not just investment products, capable of expanding the functions and coverage of traditional finance. This also marks a symbolic convergence, where digital assets and traditional finance are permeating each other to form a unified ecosystem.

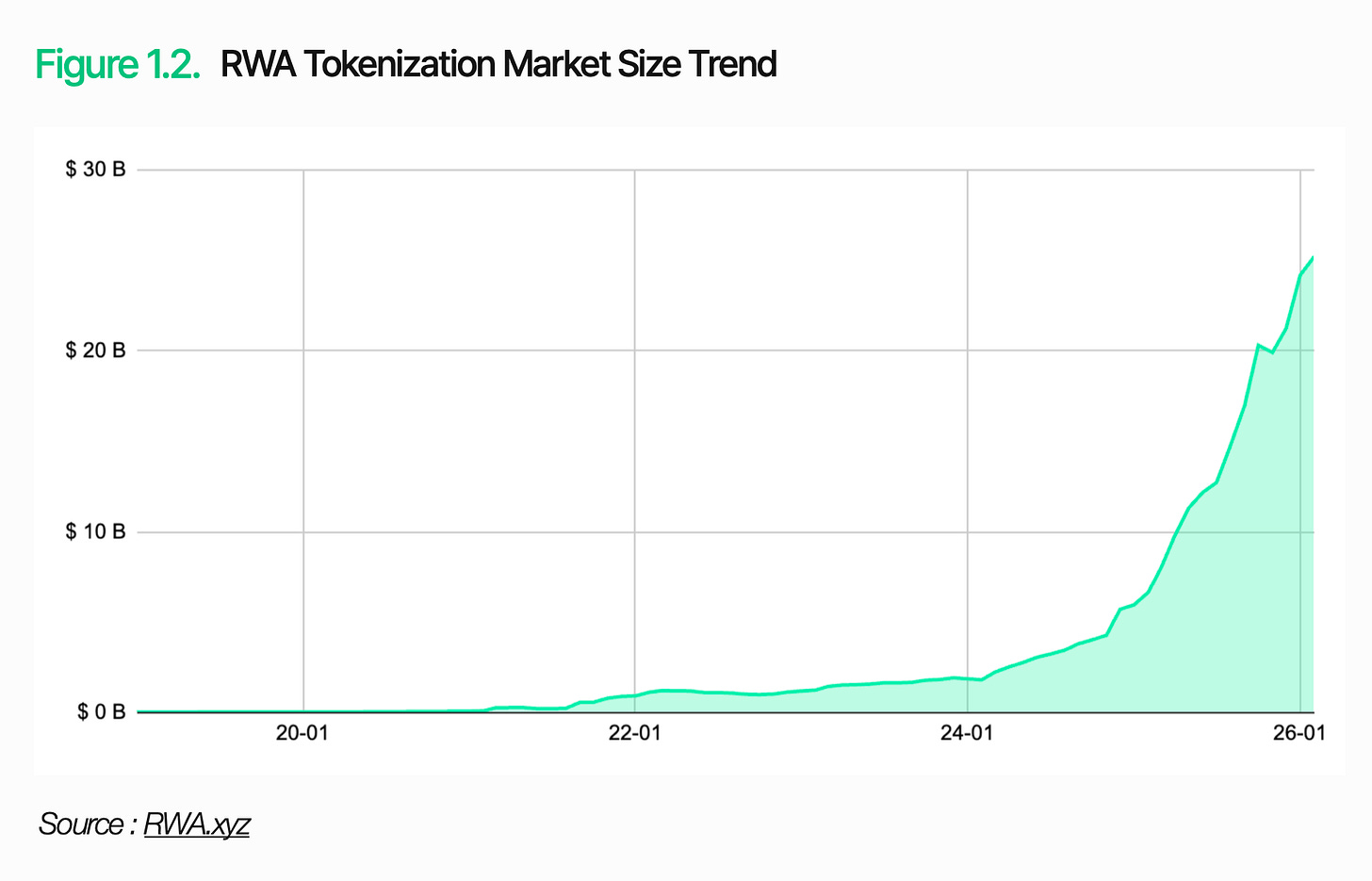

The market itself is rapidly expanding. By 2025, the annual trading volume of stablecoins is expected to reach approximately $33 trillion, a year-on-year increase of 72%. The market for tokenized real-world assets (RWA) exceeds $25 billion, with tokenized US Treasury bonds alone accounting for $10 billion. The scale of digital assets has reached a level that institutional investors cannot ignore.

2. What Digital Asset Infrastructure Needs

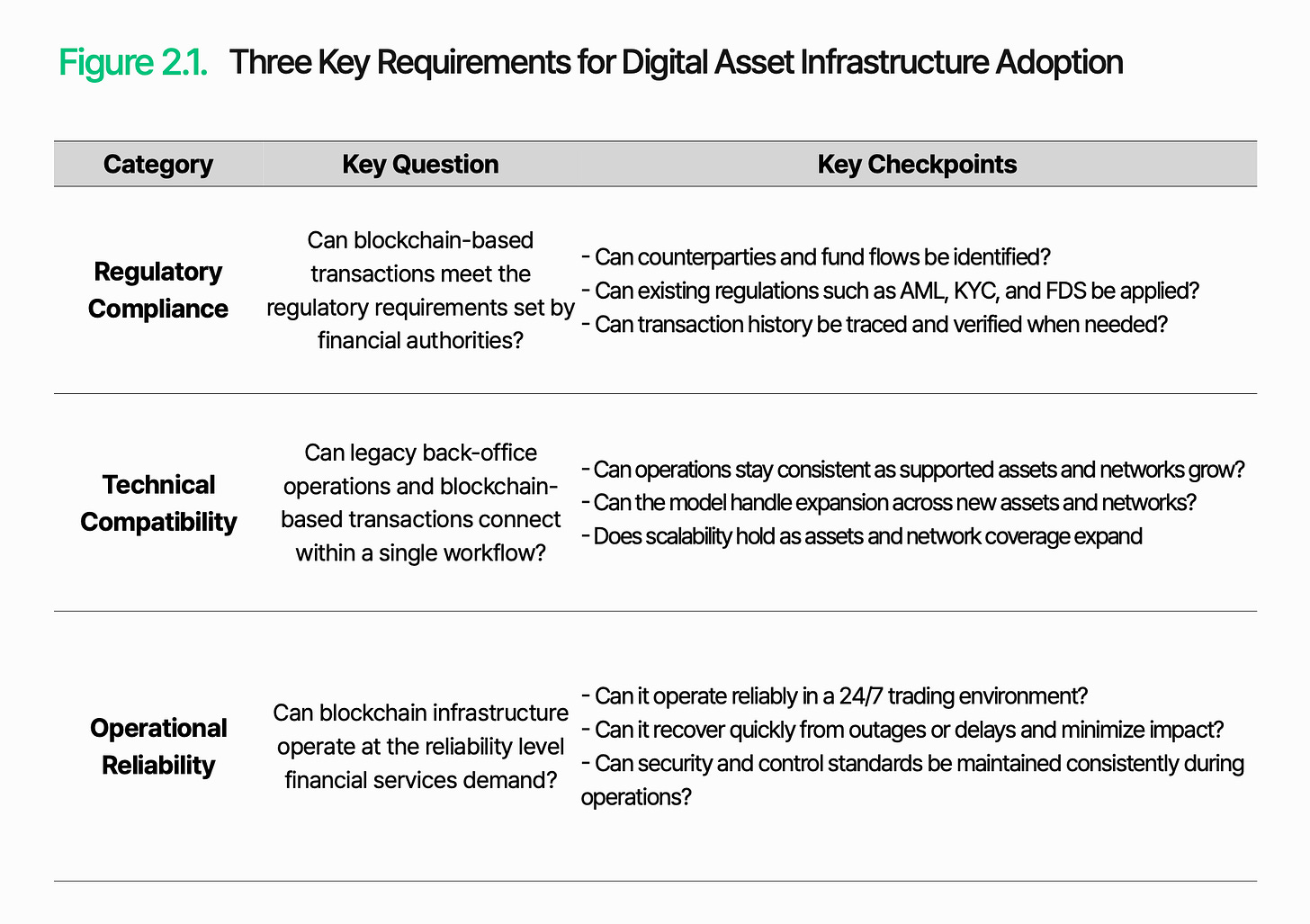

Digital assets are no longer optional; the key is how to apply them. First, it is essential to clearly understand the role of blockchain and its limitations. Blockchain is an efficient ledger technology used to securely record and verify transactions. Its role is limited to this.

To function as financial infrastructure, independent transaction processing, management, and control operating systems must be built on top of it. Before adopting this system, financial institutions must first assess three aspects: regulatory compliance, technical compatibility, and operational reliability.

2.1. Regulatory Compliance

Key Question: Can blockchain-based transactions meet the regulatory requirements set by financial regulators?

Regulatory compliance is the first hurdle faced by digital asset infrastructure. As digital assets enter the regulated financial realm, they face the same obligations as traditional finance. However, the environment in which these rules must apply is entirely different and still feels unfamiliar.

Regulations such as Anti-Money Laundering (AML), Financial Data Security (FDS), and Know Your Customer (KYC) remain in effect. The real challenge lies in how to apply these regulations. In traditional finance, real-name accounts ensure consistent identification of counterparties and the flow of funds. However, on the blockchain, the core of transactions is the wallet address, and the association between the address and the actual user is not automatically visible. Therefore, identifying counterparties and tracking the flow of funds becomes more complex.

The core of regulatory compliance is whether blockchain-based transactions can be identified and managed within the existing regulatory framework, thereby maintaining traceability of counterparties and the flow of funds, and enabling regulatory measures to be enforced.

2.2 Technical Compatibility

Key Question: Can traditional back-end operations and blockchain-based transactions connect within a single workflow?

For digital assets to serve as financial infrastructure, blockchain-based transactions must be processed within existing back-end workflows. They cannot operate independently of traditional systems.

The challenge lies in the fact that blockchain operates outside the internal systems of financial institutions. The ways these two environments record and process transactions are fundamentally different. The structural format of blockchain data cannot be directly read by traditional systems. Additionally, there are differences in data structures and interpretation methods across different networks. As the number of supported blockchains continues to grow, the scope of integration and operational complexity also increases.

Technical compatibility depends on whether blockchain data can be converted into a format that existing systems can process and whether on-chain transactions can be embedded into institutional workflows. Issuance, settlement, and clearing must seamlessly connect between traditional back-end systems and blockchain-based operations.

2.3 Operational Reliability

Key Question: Can blockchain infrastructure operate at the reliability level required for financial services?

Operational reliability is crucial because digital asset services rely on infrastructure that operates 24/7/365. In traditional finance, fixed operating hours and regular maintenance provide a natural buffer. However, in the blockchain realm, even slight delays or interruptions can directly lead to transaction delays and undermine institutional confidence.

The challenge is that blockchain-based services do not merely process transactions. Data collection, transaction processing, and system integration occur simultaneously. Any failure of a single component can affect the entire service. Transaction delays, data loss, or network interruptions can trigger settlement errors or reporting failures.

Reliability is not just about uptime. It requires maintaining transaction continuity, data consistency, event responsiveness, and security controls simultaneously. Digital asset infrastructure must go beyond mere connectivity; it must maintain that connectivity as a stable, production-grade service.

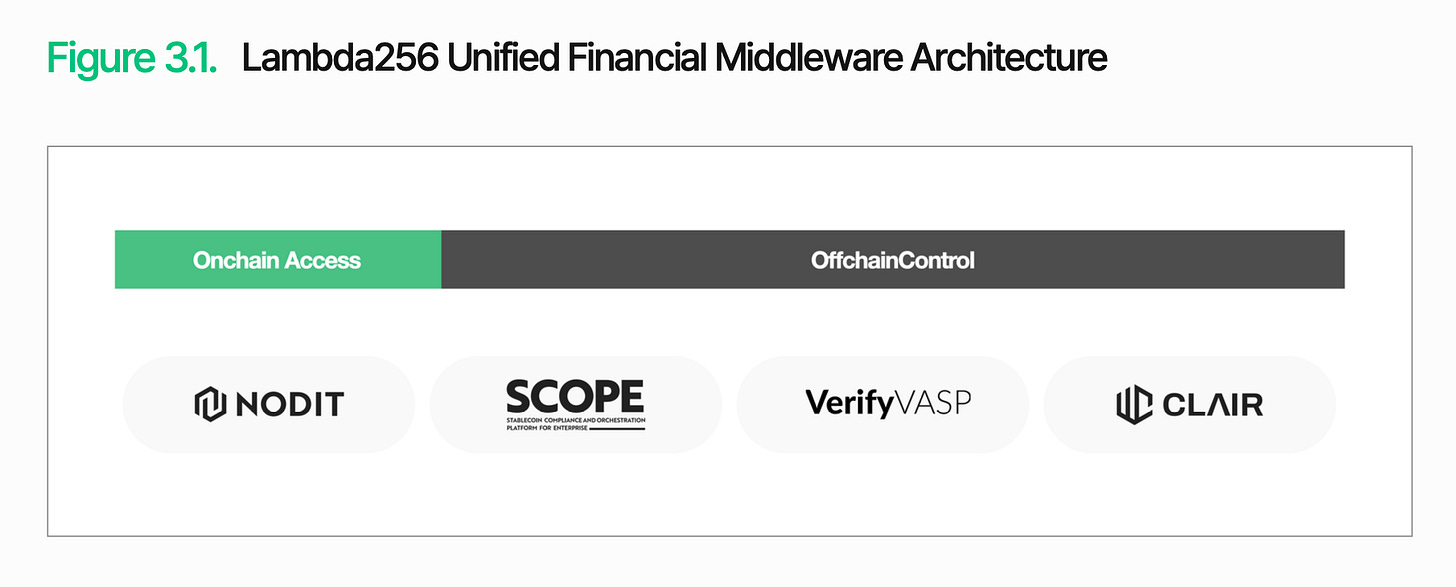

3. Lambda256: Unified Financial Middleware for Digital Asset Adoption

As mentioned earlier, the core challenge of digital asset adoption lies in how to process and manage blockchain-based transactions within the existing financial system. Lambda256 provides a unified financial middleware solution for this purpose. As a blockchain technology subsidiary of Dunamu, the operator of Upbit, Lambda256 has built a unified technology stack for digital asset adoption and possesses extensive infrastructure operation experience and rich proof of concept (PoC) experience.

The technology stack of Lambda256 consists of two layers: the on-chain access layer and the off-chain control layer. The on-chain access layer is responsible for collecting and processing data and transactions from multiple blockchains and converting them into a format usable by existing systems. The off-chain control layer is responsible for processing and managing this data within the traditional financial operational framework. The core of this architecture is to connect blockchain transactions with institutional workflows. Lambda256 provides these functions in the form of middleware, enabling financial institutions to integrate digital asset infrastructure with existing systems, thereby facilitating the deployment of digital asset infrastructure. Financial institutions can leverage on-chain advantages while maintaining operations and controls within the existing framework, reducing the burden on infrastructure and focusing more on core business.

3.1. On-Chain Access

On-chain access refers to the foundation for reliably connecting to blockchain networks, obtaining necessary data, and processing transactions. Basic functions such as balance inquiries, transaction status checks, and asset transfers rely on this layer.

However, on-chain access is not as simple as just connecting to the blockchain. Although on-chain data is public, its structure is not in a form that existing systems can directly read and use. Querying the balance or asset status of a specific wallet requires tracing related transactions and collecting the necessary information. This burden increases with the differences in data structures across different networks.

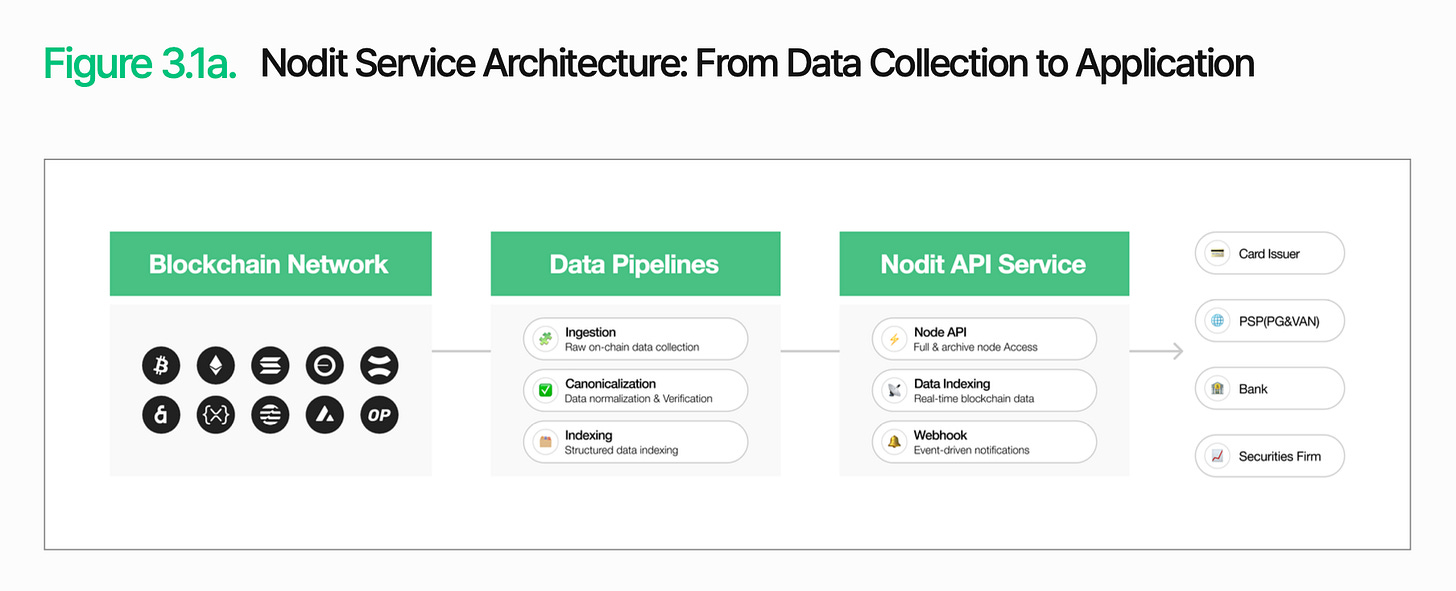

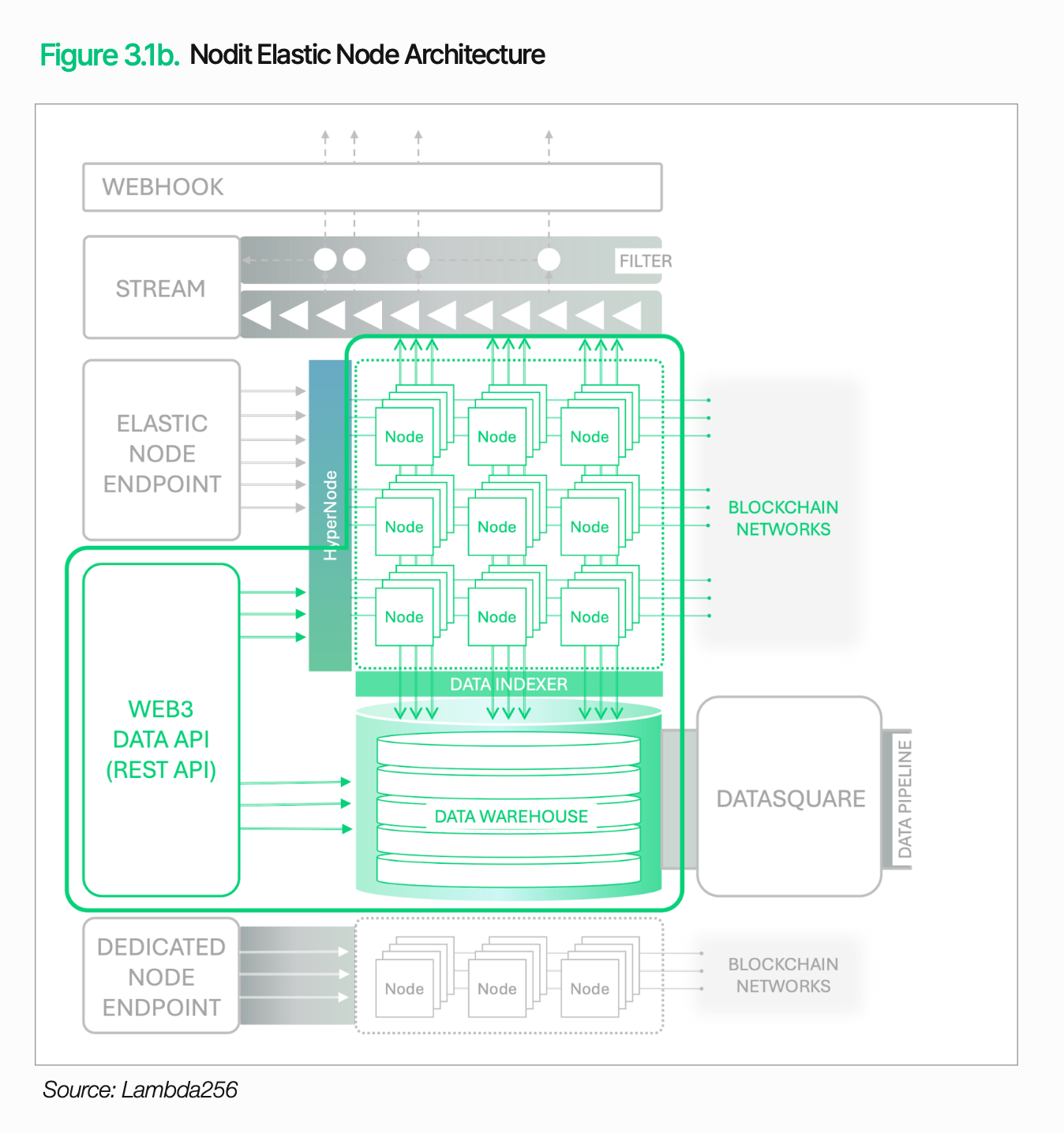

Nodit is an institutional-level blockchain data infrastructure designed to address this issue. It collects and processes data from multiple blockchain networks and delivers it in a format that existing systems can immediately use. Financial institutions can utilize on-chain data in their systems without running complex nodes or processing raw data.

Processing stability is equally crucial. Digital asset services must run continuously, and any interruption in data retrieval or transaction verification can directly lead to service delays and increased operational costs.

Nodit maintains stable processing capabilities even under high traffic conditions, thanks to its elastic node architecture (which can automatically scale nodes based on traffic) and HyperNode engine (which can distribute requests to multiple nodes). Combined with 24/7 monitoring, automatic failover, dedicated node support, and SOC 2 Type 2 certification, Nodit provides a reliable access foundation for financial institutions.

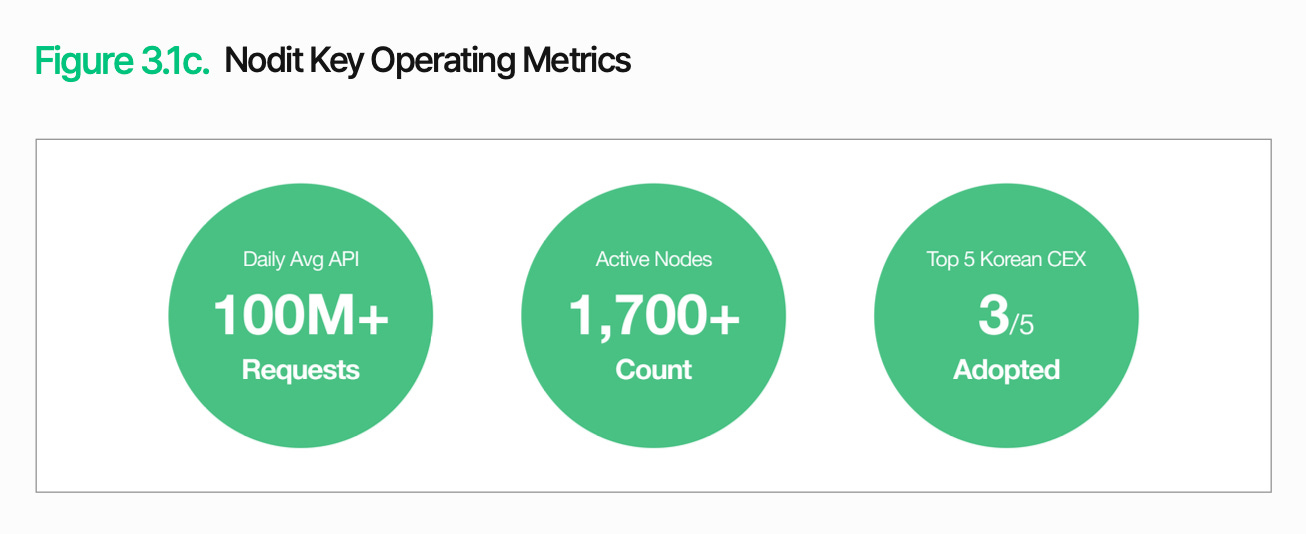

Among the top five digital asset exchanges in South Korea, Upbit, Coinone, and Korbit all operate based on Nodit's infrastructure. Its daily API request volume exceeds 100 million, with approximately 1,700 active nodes. This fully demonstrates Nodit's exceptional capabilities in high-traffic processing and stable operating environments.

The functions of the on-chain access layer go far beyond data retrieval. The data and transaction information obtained at this stage provide a shared foundation for downstream functions (including issuance, settlement, clearing, and compliance), all of which operate under the same architecture. Financial institutions can gradually expand digital asset services by integrating the required functions into existing systems and workflows without building separate infrastructures for each function.

3.2. Off-Chain Control

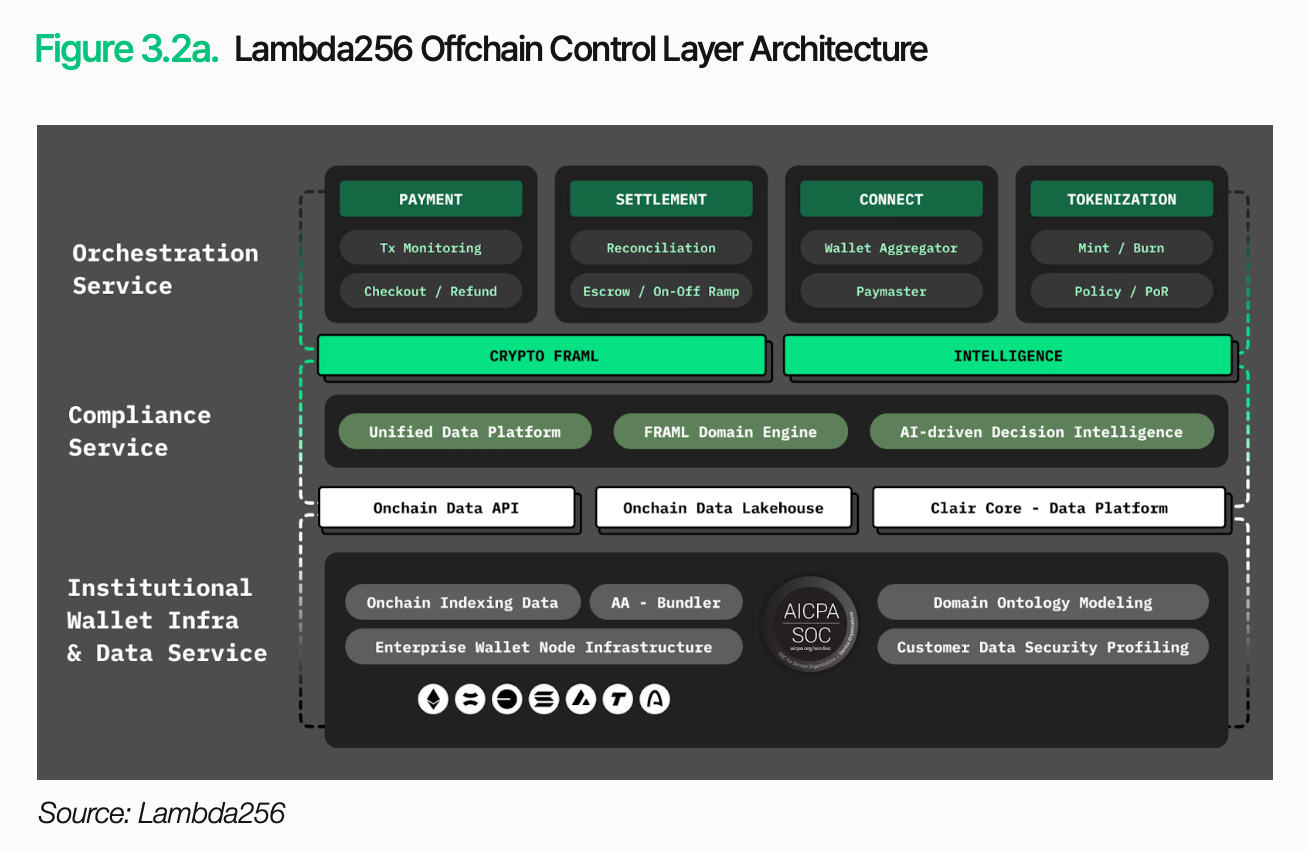

Establishing on-chain access does not mean that digital asset services are complete. Further integration of on-chain transaction results and status data into traditional financial workflows is necessary. Blockchain transactions must be processed within existing operational processes and internal control frameworks to fulfill financial service roles. Off-chain control plays this role.

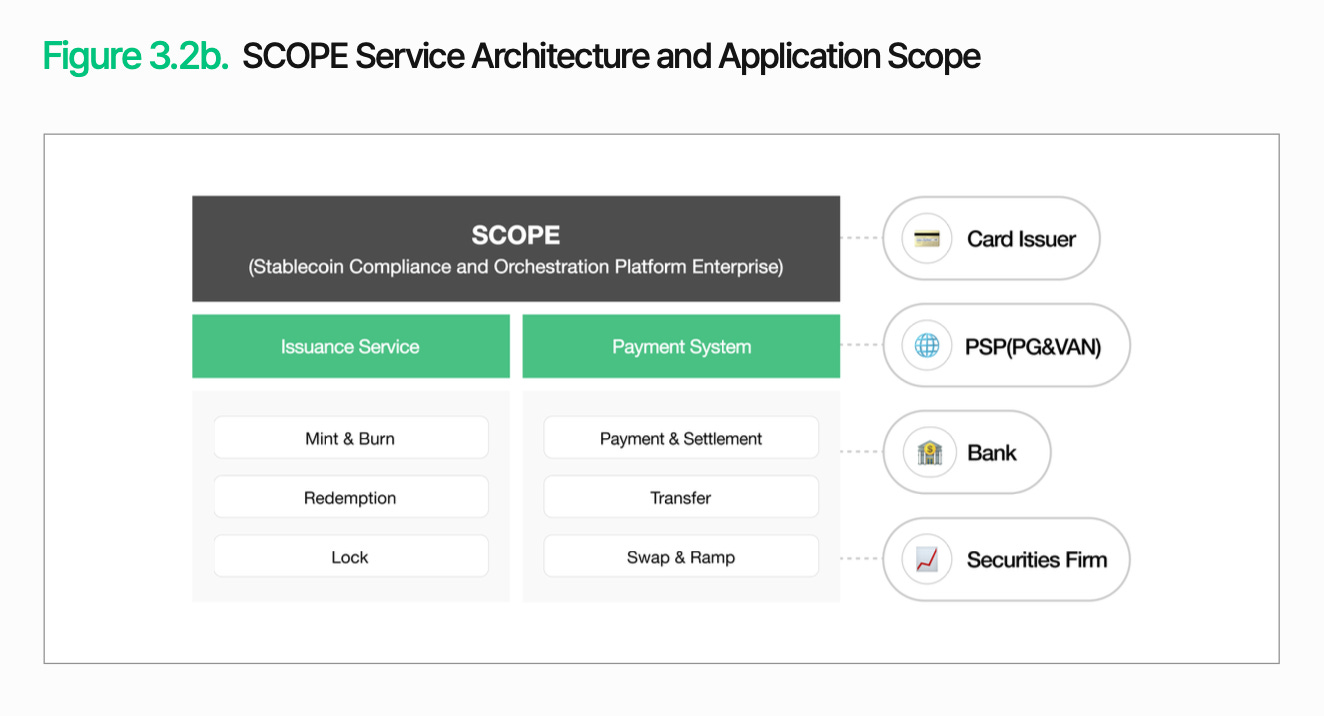

The core of off-chain control is to integrate blockchain transactions into existing financial operations. SCOPE manages issuance, distribution, settlement, and clearing within a single architecture, connecting blockchain-based transactions with traditional back-end workflows. Importantly, this does not require a complete replacement of existing systems. Institutions can gradually integrate the required functions into their existing workflows.

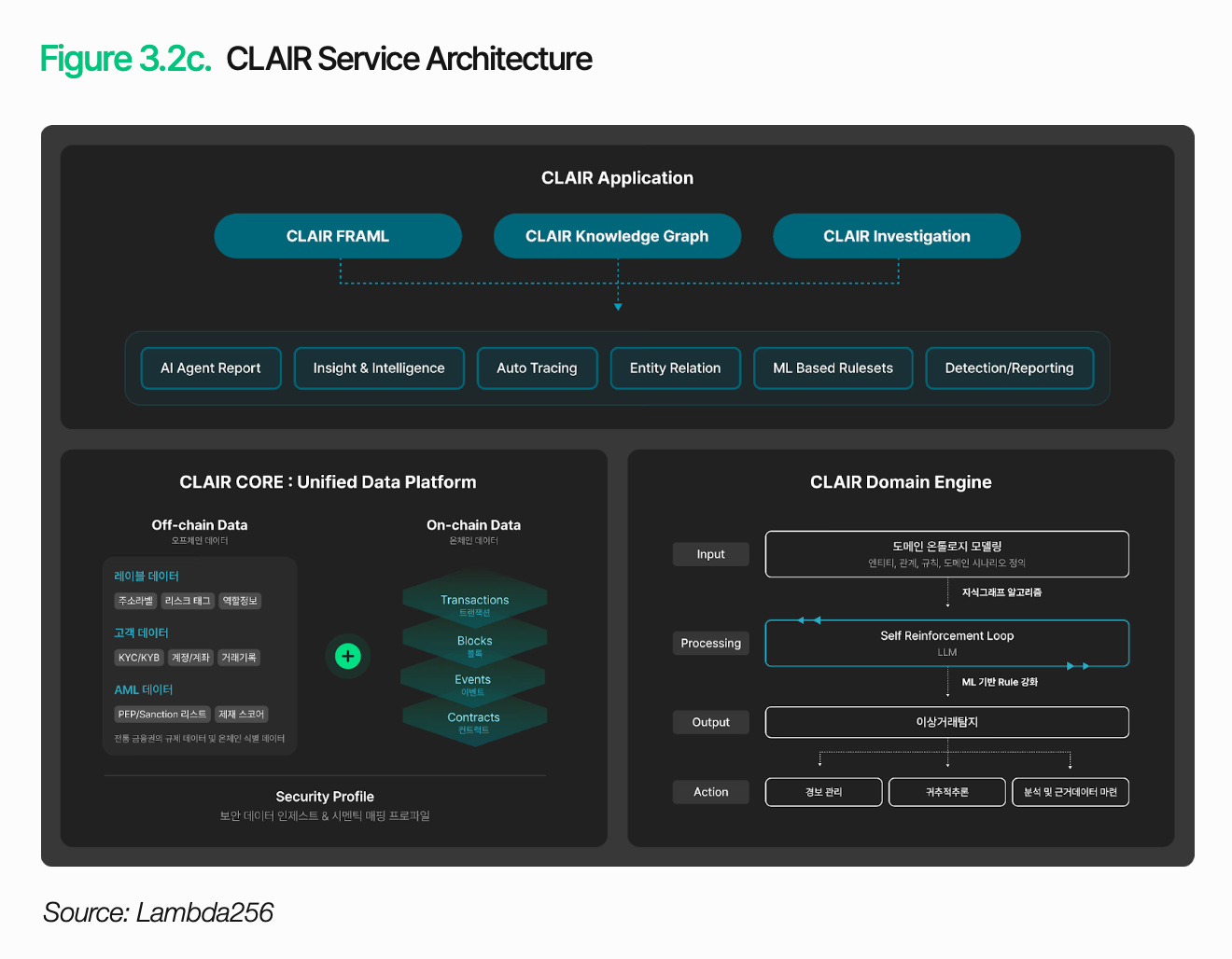

Simply incorporating transactions into operations is not enough. Institutions must also interpret the context and risks of each transaction. CLAIR analyzes the flow of funds and identifies risk signals. It maps wallet relationships through an ontology-based knowledge graph and reads contextual information of transaction patterns, enabling comprehensive tracking of funds beyond simple anomaly detection.

This functionality has been validated in practice. More than a dozen overseas law enforcement agencies and exchanges have adopted CLAIR as a white-label solution for their analytical tools. Partnerships with domestic security, auditing, and regulatory solution providers are also continuously expanding.

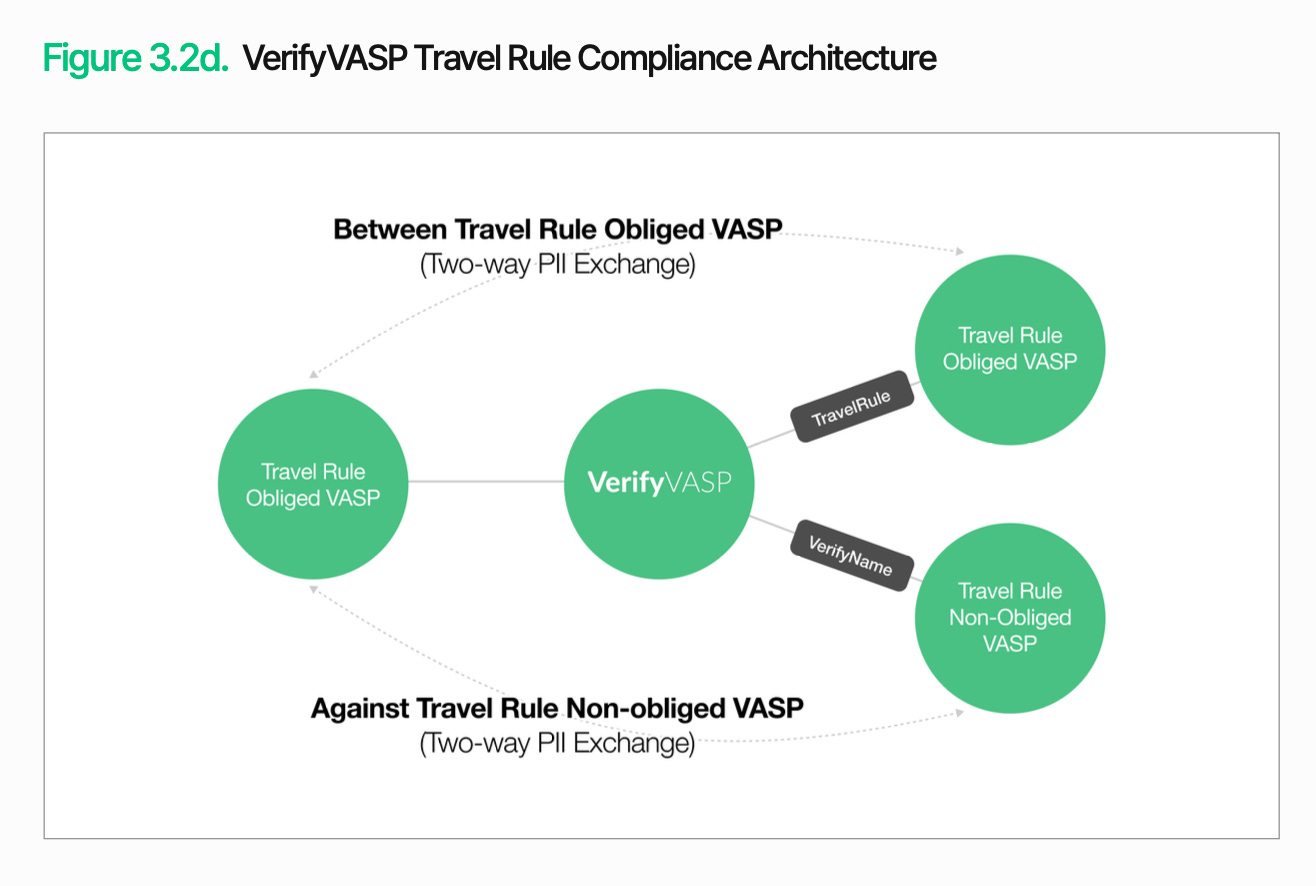

In addition to transaction monitoring, counterparty verification is also required. VerifyVASP is responsible for handling this function. To manage on-chain transactions under existing control measures, financial institutions need to verify not only the flow of funds but also counterparty information. This enables institutions to continuously and effectively manage counterparty risk without considering specific regulatory requirements.

The core of off-chain control is to enable on-chain transactions to be managed within traditional financial operations and control frameworks. Transaction execution, interpretation of fund flows, and counterparty verification must connect within a unified architecture for digital asset services to truly fulfill financial service roles. Institutions can gradually integrate the required functions based on existing systems.

4. Key Scenarios for Digital Asset Applications

The adoption of digital assets does not follow a single path. Banks, credit card companies, and securities firms will adopt different approaches based on their respective business goals and operational structures. Infrastructure needs and priorities also vary accordingly. The following sections will analyze major scenarios by industry, highlighting the challenges present and the methods to address them.

4.1 Adoption of Stablecoin Payments

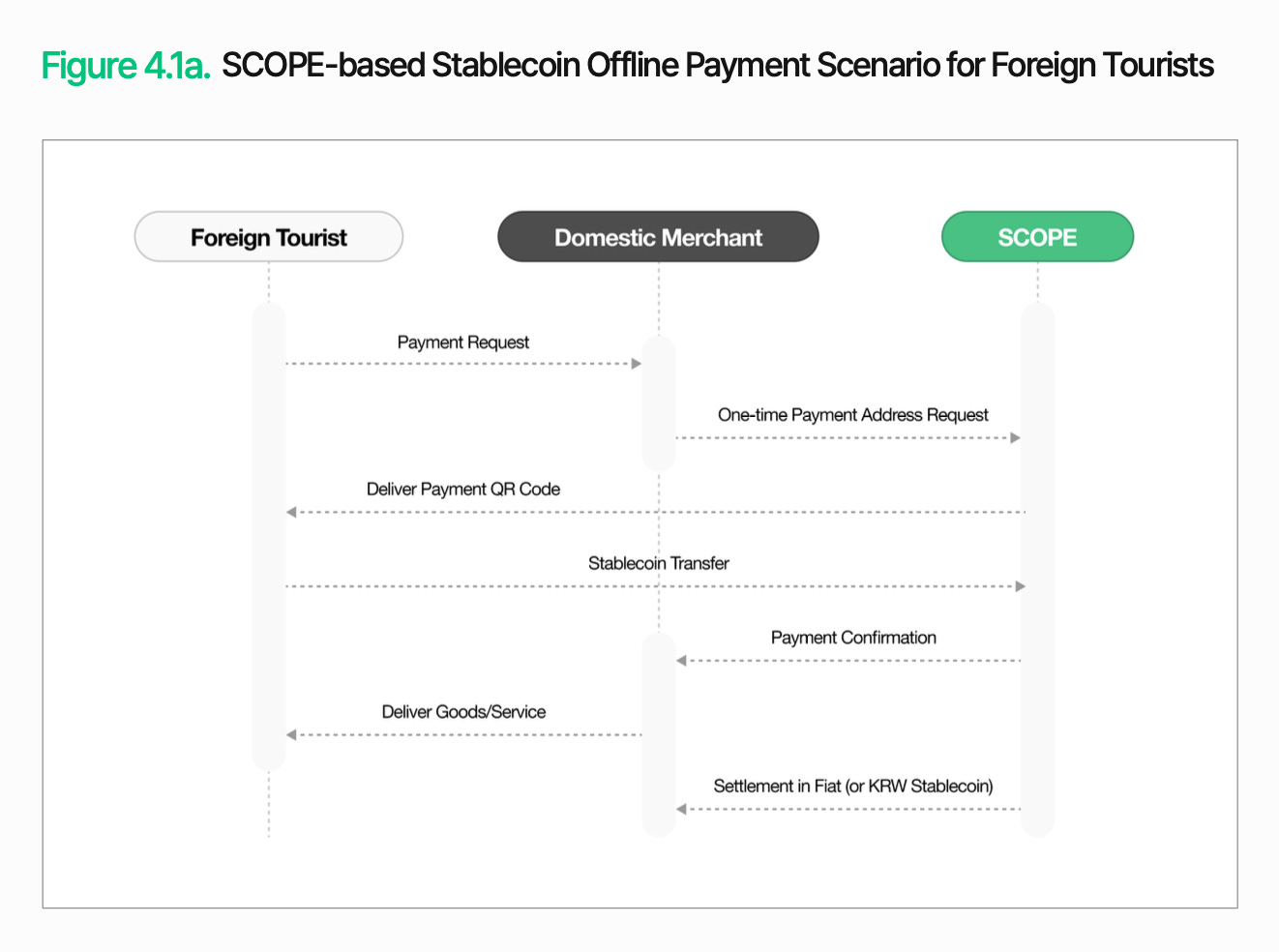

Assume a large domestic credit card company, TigerPay, introduces a stablecoin payment method for foreign tourists.

With the growth of inbound tourism, the limitations of existing payment infrastructure are becoming increasingly apparent. Cross-border card transactions incur intermediary fees and exchange rate differences, and merchant settlements take time. Tourists also bear the costs of currency exchange and the inconveniences brought by opaque exchange rates. To reduce these frictions, TigerPay aims to accept stablecoins priced in US dollars directly from tourists, while merchants receive payments in Korean won or stablecoins pegged to the Korean won.

Offline payments are relatively simple. When a merchant in South Korea initiates a payment, SCOPE generates a one-time payment address and sends it to the tourist in the form of a QR code. The tourist sends stablecoins from their wallet to that address. Upon confirmation, the merchant provides goods or services. Afterwards, the merchant receives settlement in fiat currency or Korean won stablecoins. Tourists pay with familiar digital assets, while merchants continue to use existing settlement processes.

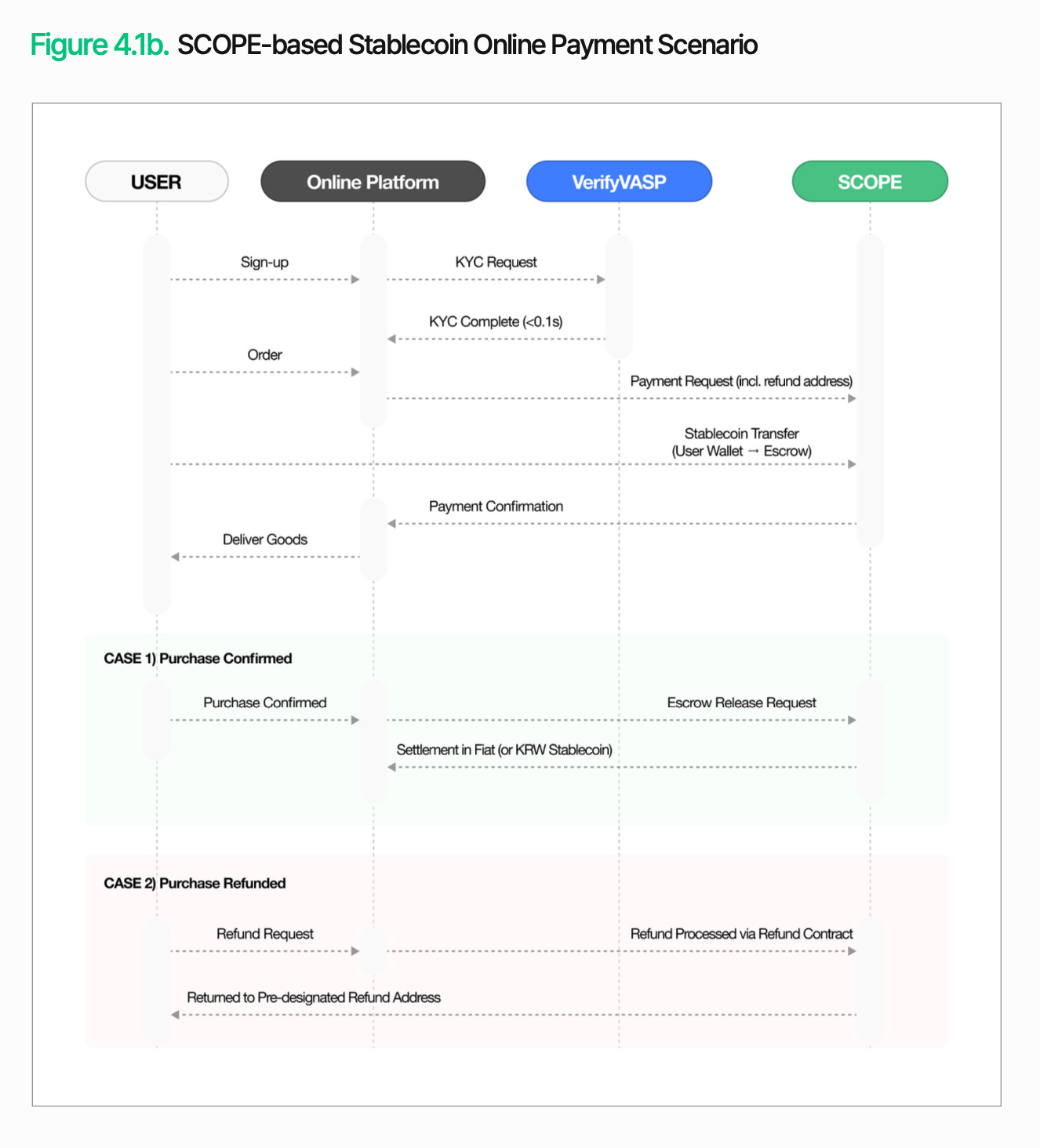

The structure of online payments is different. Since shipping and potential refunds occur between order and settlement, funds need to be temporarily held rather than immediately transferred to the seller. When a user initiates a payment, VerifyVASP performs KYC verification, and the funds are deposited into SCOPE's custody account. Once preset conditions (such as shipping confirmation) are met, the settlement process is initiated. If a refund is needed, the funds are returned to a pre-specified refund address. This allows even online transactions to complete payment, settlement, and refunds in a single process.

4.2 Security Token Issuance Platform

Assume a domestic securities firm, Tiger Securities, tokenizes a commercial real estate fund.

As the regulatory framework for security tokens gradually improves, building a Security Token Offering (STO) platform has become a practical priority for securities firms. Tiger Securities plans to tokenize its existing commercial real estate fund to attract more small investors. Under the current structure, the minimum investment threshold is high, redemptions take a long time, and the share transfer process among investors is complex. Tokenization will change this situation, allowing for the issuance of smaller denomination tokens and more flexible trading.

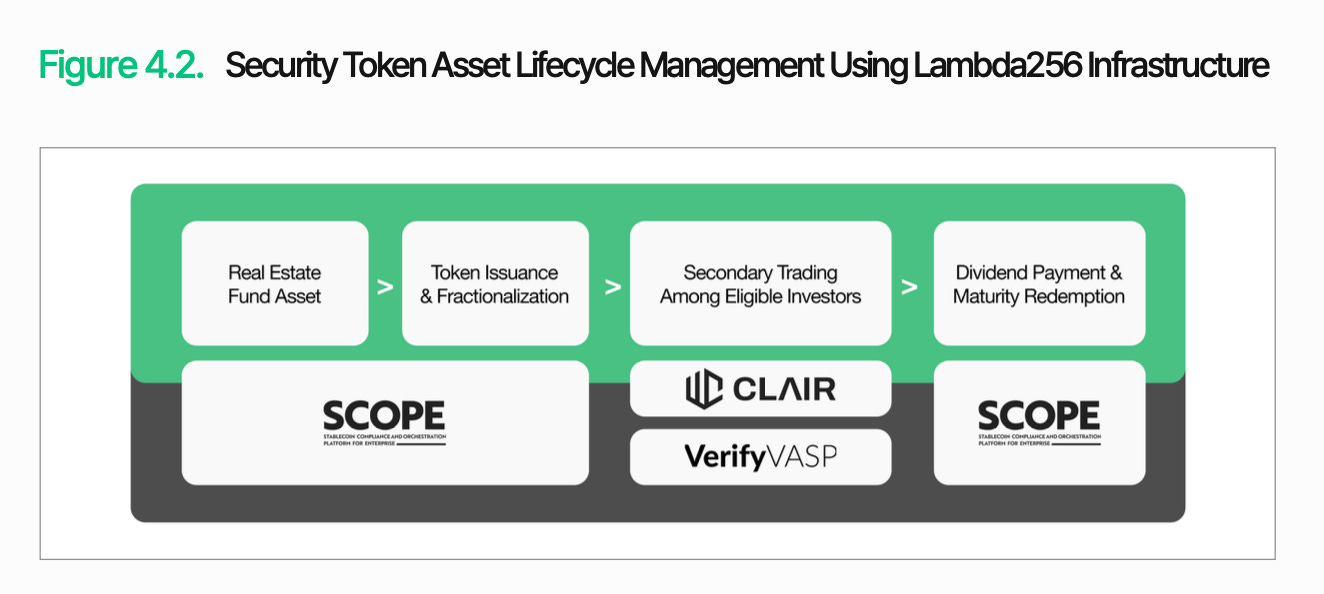

The core challenge lies not in the issuance itself but in the management post-issuance. Security tokens are classified as securities, thus requiring control over eligibility, trading conditions, and transfer restrictions throughout their lifecycle. SCOPE provides the foundation for this lifecycle management. It builds functions such as issuance, supply management, redemption, destruction, and transfer restrictions as modules. Additionally, strategies such as whitelist-based investor restrictions and transfer restrictions during lock-up periods can also be configured.

To make this architecture an operational service, data integration and regulatory responsiveness must also be in place. Nodit synchronizes on-chain data such as token balances, dividend records, and transaction histories with existing securities systems in real-time. CLAIR tracks the flow of funds and monitors abnormal transactions. VerifyVASP handles investor KYC and counterparty identity verification. During the dividend and redemption phases, SCOPE's batch payment function enables efficient allocation of funds to investors.

This architecture is not limited to a single product. Whether the tokenized assets are bonds, private equity, or commodities, the infrastructure for issuance, management, and regulatory compliance remains the same. The platform built by Tiger Securities is not a one-off system for a single product but a scalable infrastructure capable of supporting various security tokens.

5. Conclusion

The transformation has begun. Today, the gap in digital asset infrastructure is no longer about whether blockchain technology has been adopted, but whether blockchain-based transactions can truly integrate into the operations and controls of the existing financial system. The challenges faced by financial institutions ultimately boil down to three aspects: regulatory compliance, technical compatibility, and operational reliability.

Lambda256 provides a unified financial middleware solution to address these challenges. Nodit delivers blockchain data in a format usable by existing systems. SCOPE connects the issuance, transfer, and settlement of assets. CLAIR and VerifyVASP complement control and regulatory responsiveness through transaction flow analysis and counterparty verification. The significance of this architecture lies not in listing individual functions but in enabling financial institutions to gradually integrate digital asset functionalities into existing workflows.

This framework is not the final solution for digital asset infrastructure. As regulations and markets evolve rapidly, regulatory coordination, system integration, and operational reliability must be continuously refined and validated through practical applications. Nevertheless, collaborations with institutions such as the Korea Credit Finance Association and the Korea Securities Depository indicate that this approach is not just theoretical but is being reviewed and tested in real financial environments.

Ultimately, the gap in digital asset infrastructure does not depend on who adopts new technologies first, but on who can design them into an operable structure within the existing financial system and achieve a stable transition.

Latest News

ChainCatcher

3月 18, 2026 00:51:58

ChainCatcher

3月 18, 2026 00:15:35

ChainCatcher

3月 18, 2026 00:12:48

ChainCatcher

3月 18, 2026 00:11:44

ChainCatcher

3月 18, 2026 00:06:50